Putin further noted that Ukraine had lost over 90,000 troops since Kyiv’s counteroffensive against Russian forces till date…reports Asian Lite News

Ukrainian President Vladimir Zelensky has signed a decree putting into effect the decision of the National Security and Defense Council of Ukraine on financing for the country’s defense sector in 2024, Ukrainian media said, citing the presidential website.

The decree orders the government “to ensure an increase in spending on the national security and defense of Ukraine in light of the political and military situation and in compliance with the budget law requirements and to take measures to finance the operations of enterprises of Ukraine’s security and defense sector as a priority in 2024.”

As it finalizes the draft legislation on Ukraine’s 2024 budget, the government must ensure that 21.6% of GDP, or least 1.69 trillion hryvni, is allocated for the country’s security and defense needs.

Meanwhile, as the West continues to provide aid for war-torn Ukraine, Russian President Vladimir Putin stressed that Ukraine would not survive for more than “a week” without Western military and financial aid, reported Al Jazeera.

Putin made this claim on the same day when the European Union official warned that the bloc could not replace the funding gap if the US’s support dries up for Kyiv.

Earlier this week, US President Joe Biden said that he “does worry” US support for Ukraine might get derailed.

Putin while speaking at the meeting of the Valdai Discussion Club, said that Ukraine was being propped up “thanks to multi-billion donations that come each month”.

“If one just stops, it will all die in a week,” Putin said.

“The same applies to the defence system. Just imagine the aid stops tomorrow. It will live for only a week when they run out of ammo,” he added.

Additionally, Putin further noted that Ukraine had lost over 90,000 troops since Kyiv’s counteroffensive against Russian forces till date.

Moreover, while addressing a meeting of the European Political Community (EPC) in Spain on Thursday, EU foreign policy chief Josep Borrell said that the EU could not replace the US as Kyiv’s primary donor.

At a meeting of the European Political Community (EPC) in Spain on Thursday, EU foreign policy chief Josep Borrell said the EU could not replace the US as Kyiv’s primary donor.

“Can Europe fill the gap left by the US? Well, certainly Europe cannot replace the US,” Borrell said.

Moreover, the EU and the US, which includes most NATO members are crucial in Ukraine’s fight against Russia.

Over this period of time, the EU and its member states have promised over USD 100 billion of aid to Ukraine, including financing weapon deliveries.

Meanwhile, Washington has committed USD 43 billion in military assistance, whereas, Congress has approved USD 113 billion, including humanitarian aid.

However, following the weekend deal struck with opposition Republicans to avert the US government shutdown, the new US funding for Ukraine has been at a standstill.

Following the US House of Representatives on Tuesday voted to oust Republican Kevin McCarthy as Speaker, it has made the Ukraine support even more uncertain.

Hours after the short-term spending bill was passed to avoid a government shutdown, US President Joe Biden assured that Washington will “not walk away” from supporting Ukraine, CNN reported.

Dubai’s Real Gross Domestic Product (GDP) grew 2.8 percent year-on-year in the first quarter of the year to reach AED111.3 billion surpassing average global growth rates for Q1 2023…reports Asian Lite News

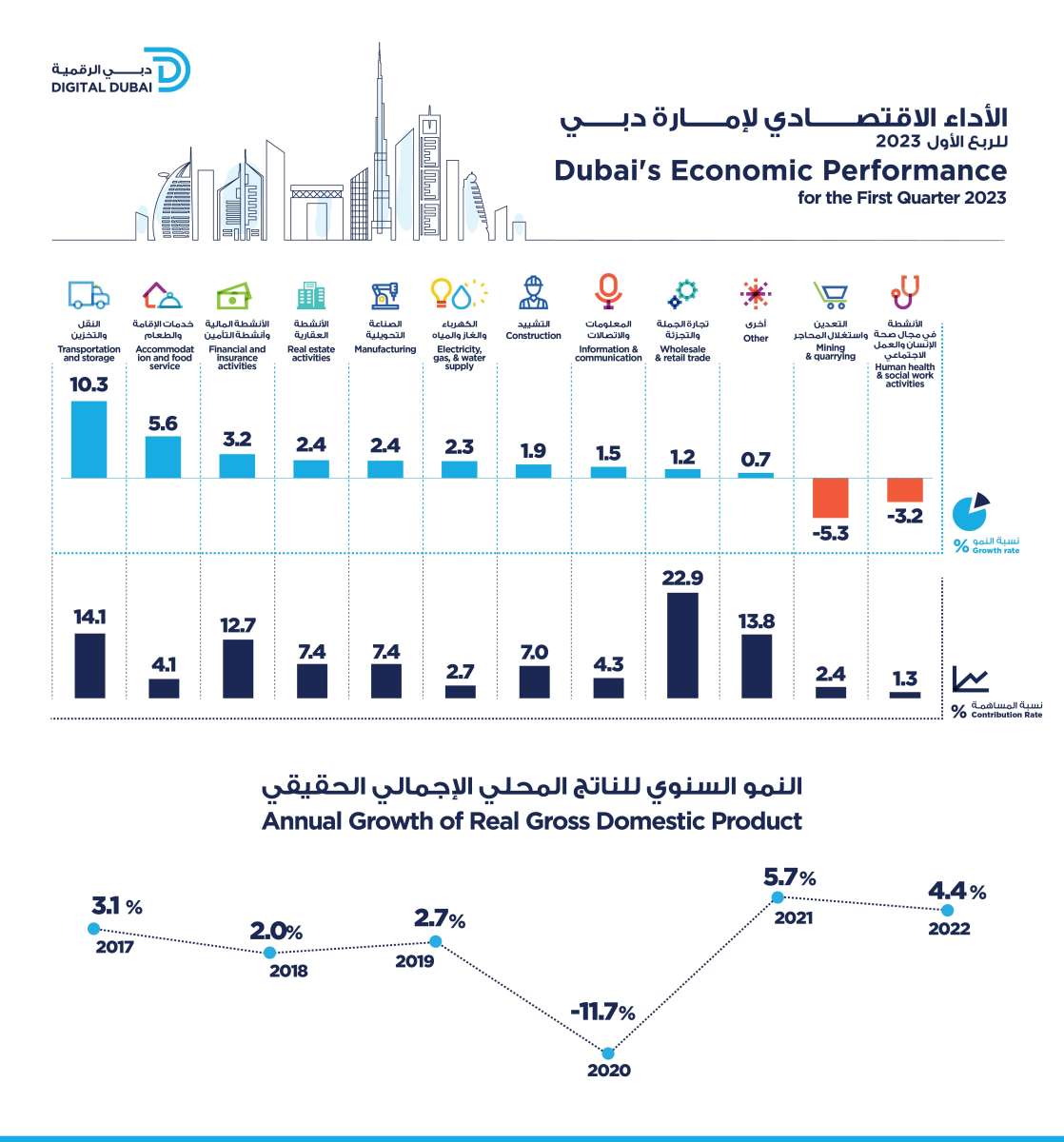

Dubai 2.8% surge maintains the robust momentum of growth achieved in 2022, when the emirate experienced a 4.4 percent expansion of the economy.

“The continued high growth in the first quarter of the year is yet another testament to Dubai’s strong fundamentals, sustainability and resilience and its capacity to constantly create fresh pathways for enterprise and innovation to flourish,” said H.H. Sheikh Hamdan bin Mohammed bin Rashid Al Maktoum, Crown Prince of Dubai and Chairman of Dubai Executive Council. “The city’s ability to sustain growth further reflects the ambitious development vision of His Highness Sheikh Mohammed bin Rashid Al Maktoum, Vice President, Prime Minister and Ruler of Dubai. Supported by its outstanding investment environment, robust infrastructure and business-enabling ecosystem, Dubai continues to outpace some of the world’s leading economies.

“The introduction of the Dubai Economic Agenda D33, which seeks to double the size of the emirate’s economy over the next decade and consolidate its status as one of the world’s top three cities, has created a strategic springboard to usher in a new cycle of growth and value creation. Powered by the harmonious partnership between the public and private sectors, Dubai will continue to raise its role in shaping the future of the global economy.”

Dubai’s growth in Q1 2023 is significantly higher than that of some of the most developed countries in the world. Data issued by the Organisation for Economic Cooperation and Development (OECD) indicate a seasonally adjusted growth of 1.6 percent for OECD countries. The European Union grew by 1.1 percent, while the US economy grew by 1.8 percent in the first quarter of the year.

The transportation and storage sector was the biggest contributor to overall growth at 48 percent. This was followed by the financial and insurance sector, which accounted for 15percent, and trade at 10 percent, according to data issued by the Dubai Data and Statistics Establishment of the Dubai Digital Authority.

Hamad Obaid Al Mansoori, Director General of the Dubai Digital Authority, said: “Dubai’s success in the economic field is an inevitable result of economic policies that express the vision of the leadership to make Dubai a leading global business and investment destination for all sectors. We at Digital Dubai will continue to work in cooperation with other government entities to ensure the sustainability of the city’s economic momentum by providing a strong digital infrastructure and the highest standards of cybersecurity, in addition to seamless access to open data, all of which will enhance the investment climate and build an environment that supports growth and prosperity.”

Helal Saeed Al Marri, Director General of Dubai’s Department of Economy and Tourism, said: “We continue to see accelerated momentum across both core sectors and new growth segments for the economy, which is being further reinforced by strong cross-industry and public-private collaboration to deliver the vision of our leadership’s 10-year Dubai Economic Agenda D33. This vision is further fortified by comprehensive strategies centered around economic diversification, entrepreneurship and the attraction of both talent and investment across sectors. This economic framework will continue to serve as a key lever for D33 as we seek to bolster Dubai’s offering as a top three global city, and the best place to invest, live, work and visit.”

The report revealed that wholesale and retail trade continued to be the largest contributor to the economy, accounting for 22.9 percent of the GDP, followed by the transportation sector, which accounted for 14.1percent. These results highlight the dynamic, diversified structure of Dubai’s economy, in which the interdependence and inter-connectedness of various sectors create synergistic growth.

Younus Al Nasser, CEO of the Dubai Data and Statistics Establishment, said: “Numbers have always been the true mirror that reflect the reality of economic activity, and today, with our entry into the era of artificial intelligence, the importance of data and statistics has increased not only in exploring the current reality, but also in foreseeing the future by analysing statistical patterns to enable decision-makers to make the right call. The data collected by the Dubai Data and Statistics Establishment reveals the significant economic progress the emirate is making, driven by the clear vision of our leadership, and the collaborative efforts of all stakeholders.”

The trade sector recorded a 1.2 percent growth in the first quarter of 2023, compared to the same period in 2022, bringing an added value of AED25.5 billion. The sector accounted for 22.9percent of the economy and contributed 10 percent of overall recorded Q1 2023 growth. It encompasses a wide range of companies dealing in various consumer and capital goods. Trade, which has a notable impact on various other activities, includes some of the largest companies in the country and the region, whose commercial activities cover a wide range of consumer and capital goods.

Transportation and storage outperformed all other sectors with a significant growth of 10.3 percent in Q1 2023, compared to the same period last year. The sector contributed 48 percent to the overall recorded first quarter growth, bringing AED15.6 billion in added value. The transportation and storage sector included activities related to land transport for individuals and goods, maritime transport, handling and storage, postal services, air transport for individuals and goods, and related supporting activities.

Air transport accounts for the largest proportion of the transport and storage sector given its sizeable production volume. The sub-sector’s performance was positively impacted by the increase in the demand for the services of national carriers, which recorded 68 percent growth in passenger numbers in Q1 2023, compared to the same period last year.

The accommodation and food services sector reported a 5.6 percentgrowth rate in the first quarter of 2023, with an added value of approximately AED4.5 billion. The sector contributed 4.1 percent to the economy and 8 percent to overall recorded growth in Q1. The emirate welcomed 4.67 million international visitors, a 18 percent increase from the 3.97 million welcomed during the same period in 2022, according to figures from Dubai’s Department of Economy and Tourism.

These results were made possible by the efforts of various initiatives of stakeholders to attract visitors, including international conferences and exhibitions throughout the year.

The Dubai Data and Statistics Establishment report revealed that real estate activities grew by 2.4percent, contributing 7.4 percent to the economy and 6 percent to the overall recorded growth, driven by the growth in real estate margins on property sales, which grew significantly in Q1 2023, according to Dubai Land Department figures.

The sector benefitted from the leadership’s directives, as well as the economic stimulus packages the Dubai Government offered, coupled by the flexibility, transparency, and confidence that the sector offers to investors and consumers.

Financial and insurance activities recorded a growth of 3.2 percent in the first quarter of 2023, contributing 12.7p ercent to the GDP and AED14.2 billion in added value. The sector accounted for 15percent of Dubai’s overall Q1 growth. Data from the UAE Central Bank indicated a 3.5 percent growth in credit balances and a 14.9 percent growth in deposit balances compared to the same period last year.

Meanwhile, other economic sectors experienced a growth rate of 1.5 percent in the first quarter of 2023, contributing a combined 35.5 percent.

The borrowing figure was £3bn lower than in April but £10.7bn higher than a year ago and the second highest May borrowing since monthly records began in 1993…reports Asian Lite News

The UK’s total government debt pile in May reached more than 100% of annual national income for the first time since 1961 as state borrowing more than doubled, according to official figures.

In a blow to Rishi Sunak’s plans to cut taxes before the general election, which is expected next year, the Office for National Statistics (ONS) said net debt reached £2.6tn as of the end of May, estimated at 100.1% of gross domestic product (GDP).

It is the first time the ratio of debt to GDP has risen above 100% since March 1961, apart from a brief spike at the height of the Covid-19 pandemic that was later revised down because of stronger GDP figures.

The increase in total debt came after government borrowing soared to £20bn in May, pushed higher by the cost of energy support schemes, inflation-linked benefit payments and interest payments on debt.

The borrowing figure was £3bn lower than in April but £10.7bn higher than a year ago and the second highest May borrowing since monthly records began in 1993.

A rise in tax receipts offset the increase in debt payments. Economists said the chancellor Jeremy Hunt’s drive to cut spending across Whitehall appeared to be having an effect. But the combination of higher income and cuts in day-to-day spending was unable to prevent a steep rise in the monthly deficit.

Hunt said the government had been taking “difficult decisions” to balance the books after the pandemic and Russia’s invasion of Ukraine.

“We rightly spent billions to protect families and businesses from the worst impacts of the pandemic and [Vladimir] Putin’s energy crisis,” he said. “But it would be manifestly unfair to leave future generations with a tab they cannot repay. That’s why we have taken difficult but necessary decisions to balance the books in order to halve inflation this year, grow the economy and reduce debt.”

Martin Beck, the chief economic adviser to the EY ITEM Club, said that while there were only two months of figures for the current financial year, borrowing was already running £2.1bn above the most recent estimates by the Office for Budget Responsibility (OBR), the Treasury’s independent forecaster.

Beck said: “We expect this gap to widen as we move through 2023-24. The likelihood that GDP and inflation will be stronger than the OBR expects is positive for tax revenues. However, this will be more than offset by the upward pressures on spending.

“Higher inflation combined with higher short- and long-term interest rates will significantly increase the level of debt interest payments, and borrowing could overshoot the OBR’s forecast by as much as £20bn by the end of the fiscal year.”

TaxPayers’ Alliance, a right-of-centre pressure group, said Hunt should respond with even deeper cuts to public spending to free up funds for tax cuts.

Samuel Tombs, the chief UK economist at Pantheon Macroeconomics, said financial markets would only tolerate the government reviving tax cuts after the debacle of last autumn’s mini-budget if inflation had fallen sharply and interest rates had “risen to a lesser extent” than the markets currently envisaged.

Provisional estimates released by NSO recently showed the overall economic growth in FY23 at 7.2%, powered by a higher-than-expected growth in the fourth quarter…reports Asian Lite News

India’s gross domestic product (GDP) reached the $3.75 trillion-mark in 2023, from around $2 trillion in 2014, Finance Minister Nirmala Sitharaman’s office said in a tweet.

India has moved from tenth to the fifth-largest economy in the world, the tweet added. Highlighting the nine years of reforms under the Narendra Modi-led government, Sitharaman’s office also said: “India is now being called a bright spot in the global economy.”

Four countries ahead of India in terms of GDP at current prices include China, United States, Germany, and Japan. India has surpassed the United Kingdom, France, Canada, Russia, and Australia in GDP numbers.

The provisional estimates released by the National Statistical Office (NSO) recently showed the overall economic growth in FY23 at 7.2 per cent, powered by a higher than expected growth in the fourth quarter.

Speaking at an Assocham event in Kochi, Chief Economic Advisor V Anantha Nageswaran said the final number could be higher than 7.2 per cent because the underlying momentum in the economy was quite strong.

While stressing that India being a low-middle-income country cannot sit on its laurels, the CEA said: “We need to catch up with the pre-pandemic trend. Even before the pandemic, the economy was slowing down in 2018-19 and 2019-20. It is important to arrest that kind of slowdown,” he said.

Nageswaran said if the country could sustain 6.5 to 6.8 per cent growth for the rest of the decade, it would be a creditable achievement on part of the Indian economy given the global conditions, while cautioning that the export growth could be a problem given the external situation.

He said India’s overall macroeconomic management had been prudent and sensible without over stretching during the pandemic, as several advanced countries did.

Talking about India’s trajectory from 10th to fifth-largest economy, the CEA also highlighted that India now contributed to one-sixteenth of the global GDP compared to one in 100 per cent about 20 years ago.

He also said the farm sector was well poised to take advantage of the kharif crop as shown in the higher tractor sales number, record wheat procurement, seed availability, and adequate food stock.

Private consumption, Nageswaran said, was at a 16-year high at 58.5 per cent of GDP. He said capital formation investment by industry was expected to pick up and gather steam.

“The last decade for industry was somewhat of a lost decade because of balance sheet problems. That has been overcome,” he said.

Nageswaran said the nominal wage growth of the agricultural and non-agricultural rural employees was in the high single digits. He said as inflation moderates to between 4 and 5 per cent, real wages would be positive in the course of FY24 as compared to FY23, which would also boost rural consumption.

The CEA also talked about structural changes in the global economy after 35 years of emphasis on globalisation in terms of geopolitical tensions and supply chains being reconfigured.

“Most of these things happen in a cyclical manner. So we have to be prepared for that. That is why we are not saying that we will be able to grow at 8-9 per cent.”

The CEA said while continuing to focus on improving the domestic economic fundamentals and the ease of living and doing business, India can reduce its dependence on global growth. “…and whatever comes through export goods will be an icing on the cake,” Nageswaran said.

The fiscal deficit for 2022-23 worked out to be 6.4 per cent of the gross domestic product (GDP), as it was projected by the finance ministry in the revised budget estimates, according to government data released last week.

Unveiling the revenue-expenditure data of the Union government for 2022-23, the Controller General of Accounts (CGA) said that the fiscal deficit in absolute term was Rs 17,33,131 crore (provisional).

The government borrows from the market to finance its fiscal deficit. CGA further said the revenue deficit worked out to be 3.9 per cent of GDP, while the effective revenue deficit was 2.8 per cent of GDP. In the Union Budget presented by Finance Minister Nirmala Sitharaman in the Lok Sabha on February 1, the fiscal deficit target for 2023-24 was pegged at 5.9 per cent of the GDP.

The delivery of the first vehicles is anticipated in 2026, with completion by 2030…reports Asian Lite News

Czech President Petr Pavel has signed a law that raises the country’s annual defence spending to at least 2 per cent of the gross domestic product (GDP), his office said in a statement.

The legislation, which will come into force in July and apply to next year’s state budget, aims to provide stable funding for costly defence projects to modernize the military, Xinhua news agency reported citing the statement as saying.

This commitment aligns with a 2006 agreement among members of the NATO, which obligates them to allocate 2 percent of their GDP on defense to maintain the alliance’s military readiness. The Czech Republic has repeatedly pledged to increase its defence spending.

The government’s plans have so far included defence spending of 130 billion Czech crowns ($5 billion). To achieve the 2 per cent target, the Defence Ministry’s budget would increase by about 21.5 billion Czech crowns in 2024, the Czech News Agency reported.

Last month, the government approved a plan to purchase 246 CV90 infantry fighting vehicles from Sweden. The deal, valued at 59.7 billion Czech crowns, was described by local media as “the largest army purchase in the modern history of the Czech Republic and one of the largest state orders ever”.

The delivery of the first vehicles is anticipated in 2026, with completion by 2030.

GDP growth at 7.2 per cent for fiscal 2023 indicates the economy has done better than expected…reports Asian Lite News

India’s gross domestic product (GDP) growth for FY23 is estimated at 7.2 per cent, the National Statistical Office (NSO) announced on Wednesday.

According to NSO, which comes under the Ministry of Statistics and Programme Implementation, the growth in real GDP during 2022-23 is estimated at 7.2 per cent as compared to 9.1 per cent in 2021-22.

The GDP growth during the fourth quarter of 2022-23 was at 6.1 per cent, NSO said.

However, economists were of the view that the numbers were higher than what was expected earlier.

The NSO said the GDP in the year 2022-23 is estimated to attain a level of Rs 160.06 lakh crore, as against the First Revised Estimates of GDP for the year 2021-22 of Rs 149.26 lakh crore. The growth in real GDP during 2022-23 is estimated at 7.2 per cent as compared to 9.1 per cent in 2021-22.

Similarly, the GDP in Q4 2022-23 is estimated at Rs 43.62 lakh crore, as against Rs 41.12 lakh crore in Q4 2021-22, showing a growth of 6.1 per cent, the NSO said.

Reserve Bank of India (RBI) Governor Shaktikanta Das, at the recent annual conference of the Confederation of Indian Industry (CII), had said there are chances of India’s gross domestic product (GDP) for FY23 crossing the estimated 7 per cent growth going by the trends.

He was confident that India’s GDP growth rate for FY24 at 6.5 per cent.

GDP growth at 7.2 per cent for fiscal 2023 indicates the economy has done better than expected. Importantly, this growth comes on a higher base – due to upward revision of fiscal 2022 data, said Dharmakirti Joshi, Chief Economist, CRISIL.

“We expect the economy to slow to 6 per cent this fiscal due to spillover to exports from a slowing world and some impact of interest rate hikes on interest sensitive segments. Even at 6 per cent, India will be the fastest growing G-20 economy this fiscal. As for agriculture output and prices, the eyes are riveted on monsoon,” Joshi said.

On the GDP numbers, Madhavi Arora, Lead Economist, Emkay Global Financial Services, said: “The better than expected GDP print for 4QFY23 is helped by healthier capital formation and more importantly, net exports which appears to be not-a-drag on growth, as usually seen in the cost given India is a net importer.”

However, weaker private consumption is still a worry albeit looks a bit difficult to fathom, when one compares robust value added growth of consumption sectors like trade, Hotels, Transport, Communication services, Arora said.

economy.

“Another anomaly was a big discrepancy print in Q4GDP along with the big gap between GDP and GVA (gross value added) growth, with GVA growth outdoing GDP with a wide margin, depicting net indirect taxes (adjusted for subsidies) de-grew. That said, overall a healthy growth print augurs well and also validates the fact that India’s growth momentum is sustained well in FY23,” she added.

According to Aditi Nayar, Chief Economist and Head – Research and Outreach, ICRA Ltd, the GDP expansion in Q4 FY2023 was appreciably higher than expected, while remaining uneven and confirming the hopes of a sequential pickup in the pace of growth of economic activity to 6.1 per cent from the bottom of 4.5 per cent seen in Q3 FY2023.

Benefitting from the positive surprise for Q4, the FY2023 GDP growth of 7.2% exceeded the advance estimate of 7 per cent by a healthy margin, she added.

With the expansion relative to the respective pre-Covid levels of FY2019 improving to a robust 17.3 per cent in Q4 FY2023 from 15.3 per cent in Q3 FY2023, the underlying momentum of the Indian economy remains healthy.

“The positive surprise in the GVA growth for Q4 FY2023 relative to our forecast was largely driven by the industrial sector. Manufacturing growth rebounded to a YoY growth of 4.5 per cent in Q4 FY2023 after having contracted in each of the last two quarter, amid an uptick in the YoY growth in manufacturing volumes as well as an improvement in margins during the quarter, partly on account of a sustained moderation in input costs,” Nayar said.

As regards the outlook for FY24, Nayar said ICRA projects growth of real GDP at 6 per cent, with a downside risk of up to 50 bps in the event that an El Nino affects the monsoon rains.

“At the same time, frontloaded capex by the GoI and the States and a rapid execution of infra projects could provide an upside to our GDP estimates for the fiscal. We foresee the nominal GDP growth at 10 per cent for FY2024,” Nayar said.

Inflation is expected to moderate in FY2024 relative to FY2023 which is a positive for household budgets and consumption. However, the rise in home loan EMIs and its impact on the budgets of urban households and their consumption demand, contraction in exports and their impact on employment, and the impact of a potential El Nino on crops, food prices and farm incomes remains to be seen, Nayar remarked.

“The Q4 growth number is a big surprise. In particular, on production side, agriculture growth at 5.5 per cent is much better than expected, despite the unseasonal rains we saw in Jan-March period. The services growth has come on expected lines, supported by robust growth in trade, hotels and financial services. On expenditure side, the major contributor to the growth is capital formation (at 8.9 per cent) driven by investment expenditure by the government. However, a mere 2.8 per cent growth in private consumption expenditure indicates waning private sector demand, which is a concern,” said Ritika Chhabra Quant, Macro Strategist – Prabhudas Lilladher PMS.

Most lead indicators at the start of 2023 continue to display resilience, with incremental data Feb-23/Mar-23 faring better than Jan-23….reports Asian Lite News

India’s gross domestic product (GDP) growth will be at 6 per cent in FY24, said credit rating agency Acuite Ratings and Research.

In its monthly commentary on the economy. Acuite said that despite the global macro economy remaining characterised by contradictions and financial system instability risks coming to the fore, the Indian economy continues to demonstrate strength and stability.

Most lead indicators at the start of 2023 continue to display resilience, with incremental data Feb-23/Mar-23 faring better than Jan-23.

“Acuite expects GDP growth to moderate but still remain healthy at 6.0 per cent in FY24,” the report said.

Acuite Ratings & Research.

According to Acuite, there is a clear distinction emerging with respect to the strength of domestic demand — which continues to display vigour, as against the impact of slowing external demand getting captured in reduced run-rate of merchandise exports (albeit in part also due to moderation in commodity prices), waning export orders within PMI and services exports coming off their Dec-22 peak (though still above trend).

“Looking ahead, challenges for domestic growth are expected to intensify in FY24 owing to — 1) a Slowdown in global growth, with the added dimension of tightness in credit conditions post the banking sector turmoil 2) Climate risks especially a warmer summer along with El Nino risks 3) Private capex remaining uneven and sluggish and 4) downside in urban leveraged consumption owing to pass-through of higher borrowing costs,” Acuite said.

According to Acuite, the moderation in inflationary pressures and the step up in public capital expenditure should continue to drive a healthy momentum in the domestic economy.

File photo shows Ukrainian President Volodymyr Zelensky attending a press conference devoted to his two years in office in Kiev, Ukraine, May 20, 2021. (Photo by Sergey Starostenko/Xinhua/IANS)

Earlier this month, the Economy Ministry slashed its forecast for the country’s GDP growth this year to 1 from 3.2 per cent estimated earlier…reports Asian Lite News

Ukraine’s GDP shrank by 29.2 per cent in 2022, state media reported, citing an estimation by the country’s Economy Ministry.

The economic decrease reflected depressed household consumption, a decline in investment activity, and negative pressure on export and import operations caused by the Russia-Ukraine war, the government-run Ukrinform news agency reported on Tuesday.

Ukraine’s GDP performance last year was better than the initially estimated decline of 30.4 per cent due to better-than-expected dynamics in the fourth quarter.

According to official statistics, Ukraine’s real GDP declined by 31.4 per cent year-on-year in October-December of 2022.

Earlier this month, the Economy Ministry slashed its forecast for the country’s GDP growth this year to 1 from 3.2 per cent estimated earlier.

Meanwhile, the Ukrainian government has approved the State Anti-Corruption Program for 2023-2025, state media reported.

The programme envisages that Ukrainian ministries, executive authorities, state enterprises, and other government agencies will have to report on the implementation of anti-corruption measures to the National Agency on Corruption Prevention, the Interfax-Ukraine news agency reported on Tuesday.

The Ukrainian government said in a statement that the programme will result in the introduction of new corporate governance standards in public sector entities, and will enhance public control over the activities of business entities partially owned by a government.

It said the Saudi GDP reached, at the current exchange rate, more than $1 trillion in 2022, for the first time in the kingdom’s history…reports Asian Lite News

The Saudi Arabian gross domestic product (GDP) grew by 8.7 per cent in 2022, the highest among G20 countries, according to a report issued by the General Authority for Statistics.

The growth exceeded the international expectation of 8.3 per cent as the maximum, and it is the kingdom’s highest annual rate in the last decade, Xinhua news agency quoted the report as saying.

It said the Saudi GDP reached, at the current exchange rate, more than $1 trillion in 2022, for the first time in the kingdom’s history.

The contribution to the growth by the crude oil and natural gas sector reached 32.7 per cent, followed by government services, 14.2 per cent, manufacturing activities except oil refining, 8.6 per cent, and wholesale and retail trade, restaurants and hotels, 8.2 per cent.

The report revealed a 5.4-per cent growth in non-oil activities in 2022, with the sector of transportation, storage and communications reaching the highest growth rate of 9.1 pe rcent, followed by manufacturing activities except oil refining, 7.7 per cent.

Saudi Arabian Crown Prince Mohammed bin Salman Al Saud recently announced the launch of the New Murabba Development Company to develop the world’s largest modern downtown in the capital of Riyadh.

The downtown will be completed in 2030 and is expected to generate 180 billion Saudi Riyals ($48.6 billion) to non-oil GDP. The project is also expected to create 334,000 direct and indirect jobs.

The project will cover an area of 19 square km to accommodate hundreds of thousands of residents. It will feature an iconic museum, a technology and design university, an immersive multipurpose theater, and more than 80 entertainment and culture venues.

The establishment of the New Murabba Development Company is one project of the Public Investment Fund, Saudi Arabia’s sovereign wealth fund, to unlock the capabilities of promising sectors, and diversify sources of income for the oil-dependent Saudi economy.

Finland’s exports will also benefit from this growth. However, the loss of Russian markets will leave a permanent gap in exports…reports Asian Lite News

Finland’s Ministry of Finance has marked down its economic prognosis for 2023. It now predicts a 0.2 per cent GDP decline. Back in September, it projected growth of 0.5 per cent.

“It is difficult to see a path on which growth does not slow in Finland. The risk of a recession is clear, but an even greater risk is remaining locked in old structures and the resulting underutilisation of resources,” Mikko Spolander, Director of the Ministry’s Stability Unit, said on Tuesday.

Finland’s GDP is expected to grow by 1.9 per cent in 2022, decrease by 0.2 per cent in 2023 and increase again by 1.2 and 1.4 per cent in 2024 and 2025, respectively, Xinhua news agency reported.

The country’s GDP began a slight decline in autumn, and weak economic performance is expected to continue over the winter, the Ministry said in a statement on Tuesday.

A broad rise in prices has cut households’ purchasing power as incomes have not kept pace with prices. However, inflation will slow in 2023 and income growth will accelerate. The economy will recover in 2024 but will not return to the growth track that was previously forecast due to the conflict between Russia and Ukraine, it added.

According to the Ministry, the economic situation in the eurozone is very similar to that in Finland. However, most eurozone countries are suffering from the energy crisis more than Finland because natural gas plays a much greater role in their energy production.

Despite the slowdown in economic growth, the growth in world trade has been brisk and will accelerate after 2023. Finland’s exports will also benefit from this growth. However, the loss of Russian markets will leave a permanent gap in exports.

The employment rate is at a record high at the end of 2022. The number of job vacancies is also quite high. In 2023, the number of employed people will decrease by about 12,000, and the unemployment rate will rise to 7 per cent. Despite the slump, the employment rate will remain strong and begin to grow again in 2024, it said.

The forecast assumes that economic sanctions and the effects of the Russia-Ukraine conflict will remain similar, the Ministry said. New developments in Ukraine may cause significant and rapidly spreading effects on the economy. Should this occur, economic employment growth would be weaker than estimated. On the other hand, the end of the conflict and the start of reconstruction would have significant positive effects on the economy.