Governor Das highlighted the rapid expansion of digital technologies in India over recent years, citing their transformative impact on the country’s financial system…reports Asian Lite News

The Unified Payments Interface (UPI) has revolutionized India’s digital payment ecosystem and played a pivotal role in driving financial inclusion by bringing millions of unbanked individuals into the formal financial system, said RBI Governor Shaktikanta Das here on Monday.

The RBI Governor was delivering the keynote address at the Grand Finale of the G20 TechSprint 2023 here.

Das said, “A landmark example of our commitment to innovation is the UPI, which has been a game changer for India’s Digital payment ecosystem. It has helped to drive financial inclusion by bringing millions of unbanked individuals into the formal financial system”.

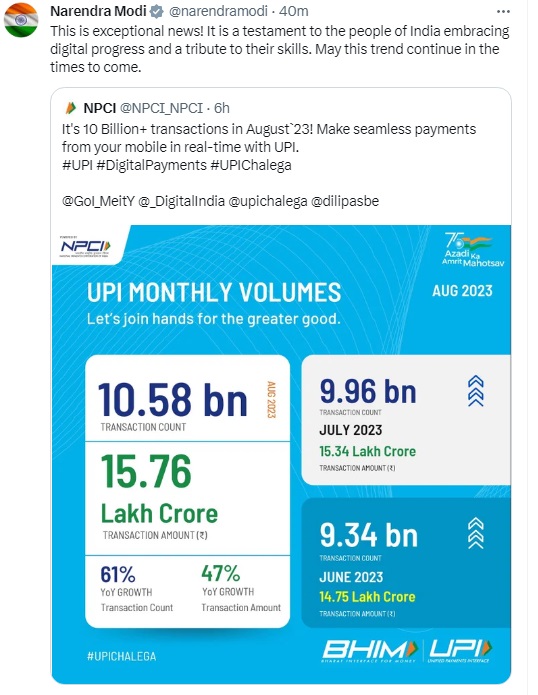

Governor Das shared that in August 2023, the total number of transactions on the UPI platform exceeded an impressive 10 billion transactions, solidifying its position as the backbone of digital payments in India. He further noted that more than 70 mobile apps and over 50 million merchants across India now accept UPI payments.

In his address, Das commended India’s thriving startup ecosystem, its vibrant talent pool, and the unwavering commitment to digital transformation. India, he emphasized, is focusing on leveraging technology to bridge gaps, empower individuals, and promote financial inclusion.

The RBI Governor said, “TechSprint 2023 resonates profoundly with India’s commitment to innovation. With its robust startup ecosystem, vibrant talent pool and unwavering commitment to digital transformation, India is now focusing on the way technology can be harnessed to bridge gaps, empower individuals and promote financial inclusions”.

Governor Das highlighted the rapid expansion of digital technologies in India over recent years, citing their transformative impact on the country’s financial system.

He noted that India’s robust digital public infrastructure, including Aadhaar, affordable internet access, and widespread mobile phone services, has enabled more people, regardless of their location or social status, to access financial services.

“The past few years have seen rapid expansion of digital technologies in India having a transformative impact on our financial system. Today more and more people have access to financial services regardless of their location or social status weighing to the robust digital public infrastructure like AADHAR, affordable internet and mobile phone services”, said Das.

The Governor emphasized that India’s journey embodies innovation with a human touch, spanning financial inclusion, digital payments, and the use of artificial intelligence for credit assessments.

The Reserve Bank of India is committed to promoting responsive innovation and has taken strategic steps in this direction, including the establishment of the Fintech Department within the RBI to manage the evolving fintech sector and the Reserve Bank Innovation Hub, a wholly-owned subsidiary engaged in technology-based projects aimed at benefiting the masses.

“At the Reserve Bank we are committed to promoting responsive innovation, as a part of this we have taken a few strategic steps in the recent past. On the institutional front we have set up the Fintech Department within the reserve bank with the objective of paying dedicated attention to the fast-evolving fintech sector”, said Das.

Governor stated, “The mandate of this department is to promote innovation while managing the associated risk if any. Similarly, we have set up the reserve bank innovation hub as a wholely owned subsidiary which is currently engaged in several technology-based projects touching the people at the bottom of the pyramid.”

Under India’s G20 Presidency, the RBI and the BIS Innovation Hub have jointly launched the G20 TechSprint, a global technology competition focused on improving cross-border payments.

This year’s edition, the fourth in the series, seeks innovative solutions for three problem statements: addressing illicit finance risks through AML/CFT/Sanctions technology, enabling settlement in emerging market and developing economy (EMDE) currencies, and developing technology solutions for multilateral cross-border CBDC platforms.

Efficient cross-border payments are vital for enhancing economic cooperation and activities between countries, and the G20 TechSprint aims to demonstrate how technology can address challenges in this domain, foster innovation, and promote seamless payments across borders while preserving financial integrity. (ANI)

ALSO READ-RBI Governor meets World Bank President during G20 meet