Tesla and SpaceX CEO Elon Musk said his companies are looking to invest in India soon.

Tesla and SpaceX CEO Elon Musk on Friday congratulated Prime Minister Narendra Modi on his re-election for a record third term to run the country.

In a post on X, the tech billionaire said his companies are looking to invest in the country soon.

“Congratulations @narendramodi on your victory in the world’s largest democratic elections,” Musk wrote.

“Looking forward to my companies doing exciting work in India,” he added.

In April this year, Musk postponed his proposed visit to India due to “very heavy Tesla obligations”.

He was expected to visit the country on April 21 and 22 and meet Prime Minister Narendra Modi.

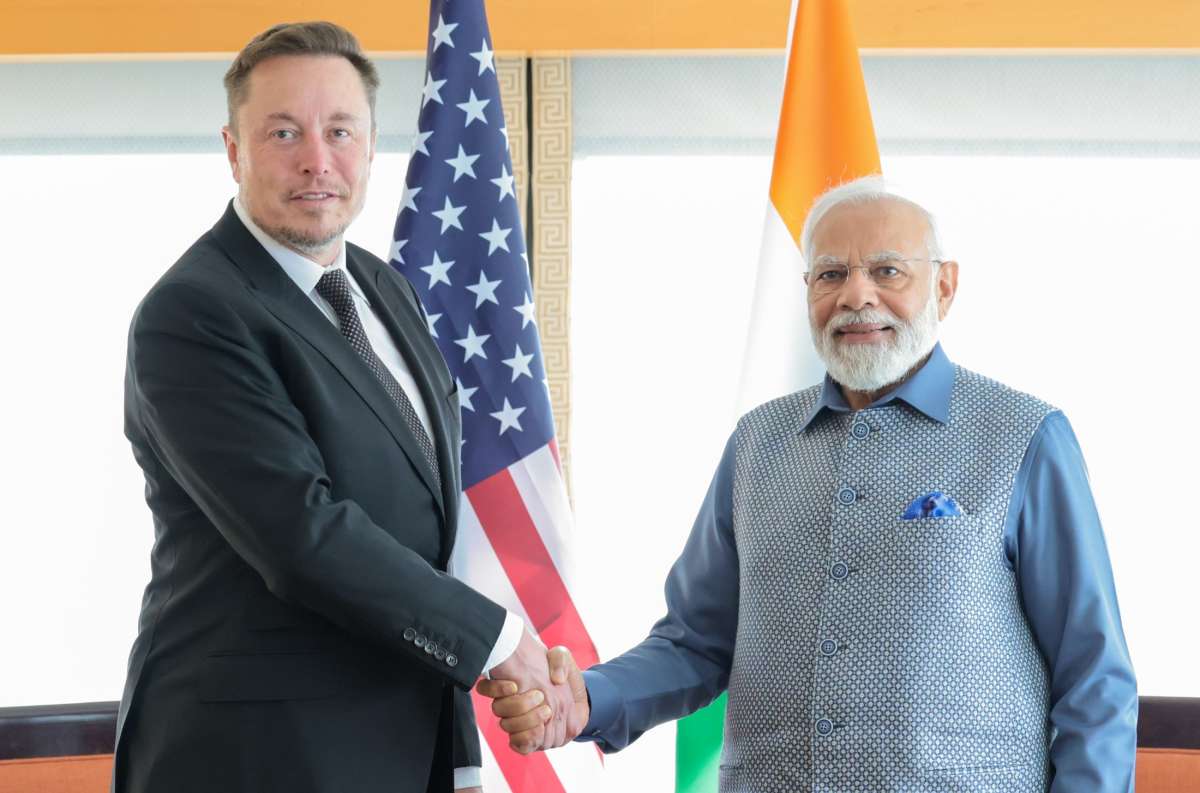

Prime Minister Narendra Modi with the CEO of Tesla Motors, Elon Musk, in San Jose, California. (File Photo)

Musk later said he looks forward to coming to India later this year.

“Unfortunately, very heavy Tesla obligations require that the visit to India be delayed, but I do very much look forward to visiting later this year,” Musk posted on X.

Musk met PM Modi in June last year in the US, expressing confidence that Tesla would enter the Indian market soon, along with Starlink.

Tesla is likely to set up its manufacturing unit in India and make large-scale investments.

Last year, Tesla approached the Indian government seeking duty cuts to import its vehicles in the country.

Savings Deposits in banks have been on a consistently upward trajectory in recent years… reports Asian Lite News

According to recent statistics from the Central Bank of the UAE (CBUAE), savings deposits in the UAE banking sector, excluding interbank deposits, grew by 10.2 percent annually, reaching AED270.48 billion at the end of January 2024 compared to approximately AED245.54 billion in January 2023, attracting around AED25 billion.

The local currency, the dirham, accounted for the largest share of savings deposits, about 82 percent or AED222.01 billion, while the share of foreign currencies amounted to 18 percent or AED48.4 billion.

Savings Deposits in banks have been on a consistently upward trajectory in recent years, rising from AED152 billion at the end of 2018 to AED172.2 billion in 2019, and reaching AED215.2 billion in 2020, AED241.8 billion in 2021, and AED245.8 billion in 2022.

The Demand Deposits increased to AED1.001 trillion at the end of January 2024, with an annual growth rate of 9.5 percent compared to AED914.74 billion in January 2023, an increase equivalent to AED86.6 billion.

Demand Deposits total comprised AED720.55 billion in the local currency, the dirham, accounting for 72 percent, and around AED280.8 billion in foreign currencies, accounting for 28 percent.

Demand Deposits continued to grow in recent years, rising from AED577.6 billion at the end of 2018 to AED599.6 billion at the end of 2019, AED696.8 billion at the end of 2020, AED848 billion in 2021, and AED907.3 billion in 2022.

According to the Central Bank’s bulletin, Time Deposits reached AED796.9 billion at the end of January 2024, with a 30.3 percent annual increase compared to about AED611.69 billion in January 2023, an increase of AED185.2 billion.

The local currency, the dirham, accounted for the largest share of time deposits, about 60 percent or AED474.88 billion, while the share of foreign currencies amounted to about 40 percent or AED322.04 billion.

In 2023, the private sector continued its strong growth, reaching AED 338.9 billion, up 35% compared to 2016. Supported by private sector and family-owned businesses, Abu Dhabi non-oil sectors is going from strength to strength…. reports Asian Lite News

The Abu Dhabi Department of Economic Development (ADDED), in collaboration with the Abu Dhabi Investment Office (ADIO), organized the second edition of the Al Multaqa quarterly meetings, aiming to strengthen partnerships with the private sector and family offices. The meetings provided the business community with updates on the Emirate’s economy and achievements in 2023, while also emphasizing future opportunities.

Launched in Q4-2023, Al Multaqa Meetings empower Abu Dhabi’s to accelerate economic growth, by providing a platform for ongoing dialogues to support investment and the development of new policies that further enhance the Emirate’s business environment. In 2023, the private sector continued its strong growth, reaching AED 338.9 billion, up 35% compared to 2016. Supported by private sector and family-owned businesses, Abu Dhabi non-oil sectors is going from strength to strength, recording a growth of 9.1 per cent during 2023 to AED 610 billion to contribute 53.4% of total real GDP.

Addressing Al Multaqa meeting, Ahmed Jasim Al Zaabi, Chairman of the Abu Dhabi Department of Economic Development (ADDED), said: “The importance of our collaborative efforts is reflected in Abu Dhabi’s growth indicators. Remarkably, we managed to achieve this strong performance despite global challenges, reflecting the strength and resilience of our ‘Falcon Economy’ and its ability to soar to new heights.” “Backed by decades-long experience, the private sector and family-owned businesses in Abu Dhabi continue to contribute to economic diversification as evidenced by their share in the highest growing non-oil sectors”.

Family-owned businesses in Abu Dhabi represent 50 per cent of companies in the construction sector, which grew by 13.1 per cent in 2023 compared to 2022, reaching more than AED97 billion; 60 per cent in the finance sector, which rose by 25.5 per cent to AED79 billion; 80 per cent in the wholesale trade sector, which achieved a growth of 7.9 per cent, to reach AED63 billion; and 70 per cent in the transportation sector, which rose by 17.1 per cent during past year.

Al Zaabi added: “In our first meeting, we underlined the crucial role that family offices and private sector play in Abu Dhabi and the UAE’s success. Today, I reiterate the importance of discussing promising opportunities, analyse challenges, and work together to overcome them. We are organising these meetings to ensure the exchange of opinions and to benefit from the extensive experiences and knowledge.”

Abdulla Gharib Alqemzi, Acting Director General of the Statistics Centre – Abu Dhabi, delivered a comprehensive presentation about economic performance of the Emirate during the past 10 years, which saw a 28.5 per cent growth of non-oil GDP, from AED 474.6 billion in 2014 to AED 610 billion in 2023, and a 19 percent rise of total real GDP, from AED 960.1 billion in 2014 to AED 1.14 trillion in 2023.

Alqemzi highlighted major sectors contributing to economic diversification efforts, including manufacturing, construction, finance, trade, transportation, real estate, and ICT.

Abu Dhabi Investment Office (ADIO)’s Musataha Programme revealed several investment opportunities offered to the private sector, enabling investors to develop government-owned land. ADIO also announced investment opportunities in the sports field in different areas of the Emirate in addition to new sites that will be offered to develop feed-selling markets.

ADIO has signed agreement with Dustour Marine Wooden Boats Trading Est. to establish a new state-of-the-art project to support the Emirate’s coastal development in line with urban, social, recreational, and economic expansion plans.

ADDED’s Industrial Development Bureau (IDB) and SMEs sector shared significant updates to further improve ease of doing business and enable the private sector to benefit from ample opportunities provided by development plans.

The IBPC-SCCI meeting highlighted facilitative measures and investment opportunities for Indian firms in Sharjah, emphasising the crucial role of periodic gatherings for communication between stakeholders.

The Indian Business and Professional Council, affiliated with the Sharjah Chamber of Commerce and Industry (SCCI), has conducted an extensive business meeting to discuss ways to strengthen cooperation and boost bilateral trade volume and mutual investments between the business communities of Sharjah and India.

Discussions delved into prospects for enhancing coordination between the two business communities and exploring investment opportunities across diverse strategic economic sectors.

The meeting also focused on bolstering the exchange of information regarding investment prospects and building sustainable partnerships to fuel growth in trade exchanges and joint investments, leveraging the comprehensive economic partnership between the UAE and India.

Held during the Ramadan suhoor banquet at Sharjah’s Jazerat-al-alam, the meeting was attended by Dr. Khaled Omar Al Midfa, Chairman of Sharjah Media City (Shams), and Ahmed Obaid Al Qaseer, CEO of the Sharjah Investment and Development Authority (Shurooq), as well as Adel Al Ali, Group Chief Executive Officer of Air Arabia, and Abdul Aziz Al Shamsi, Assistant Director-General for Communication and Business Sector at SCCI.

Also present were Satish Kumar Sivan, Consul General of India in Dubai and the Northern Emirates; Jamal Saeed Buzangal, Director of the Media Department at SCCI; Lalu Samuel, Chairman of the Indian Business and Professional Council, along with members of the Indian Business Council, business community representatives, and heads of major Indian companies operating in Sharjah.

The meeting underscored the facilitative measures and investment prospects extended to Indian companies within the emirate, emphasizing the pivotal role of periodic gatherings in bridging communication between investors, corporate heads, and business leaders from both Sharjah and India.

Moreover, the discussions highlighted the level of investment cooperation and the diverse opportunities available for Indian companies operating in Sharjah, particularly within strategic sectors such as energy, maritime industries, shipping services, and ship agencies. The meeting also delineated opportunities available for Indian companies specializing in commerce, food industries, tourism, real estate, and contracting.

Abdul Aziz Al Shamsi emphasised that the Indian Business Council’s meeting, which brought together all those concerned with consolidating ties between Sharjah and Indian business communities, stands as an essential component of the endeavours made by the Sharjah Chamber and its associated business councils to boost business relations between the two communities.

Stressing its pivotal role in catering to the needs of member companies affiliated with the Indian Business and Professional Council, Al Shamsi added that the meeting aligns with broader efforts to enhance economic and commercial cooperation with India.

He pointed out that such gatherings provide fruitful opportunities for fostering new business partnerships between Indian and Emirati companies, which in turn serve as a fundamental pillar for fortifying bilateral trade and mutual investment.

For his part, Lalu Samuel noted that the Indian Business Council’s meeting aimed at bringing together leaders of Indian companies investing in Sharjah with their counterparts in the emirate, along with relevant entities, to develop cooperative relations and explore further opportunities to achieve the council’s objectives.

Underscoring the importance of fostering communication bridges between Indian companies and economic prospects in Sharjah, Samuel clarified that this initiative seeks to cement sustainable collaborative ties and create avenues for acquainting with efforts supporting investors, and thereby elevating economic activities in the emirate.

An estimated 17,500 Indian companies are currently operating in the Emirate of Sharjah, according to SCCI’s members. The Sharjah Chamber inaugurated the Indian Business and Professional Council in February 2023.

Through informed decision-making and strategic planning, women can unlock the full potential of their investments, ensuring a prosperous future for themselves and future generations. Here are four essential tips women must consider while investing outlined by Swati Saxena, Founder and CEO of 4 Thoughts Finance…reports Asian Lite News

In today’s dynamic financial landscape women emerge as influential investors, reshaping conventional perceptions and forging their path to economic empowerment.

Despite encountering challenges like financial literacy gaps and gender biases, women demonstrate resilience and skill in navigating the intricacies of the marketplace. From managing household finances to exploring equity markets, they bring a unique perspective driven by emotional intelligence and long-term vision.

Recognizing the significance of financial planning, there is a growing call to address barriers and create inclusive opportunities. By embracing their financial journey as a nurturing process, women can craft portfolios aligned with their values, aspirations, and risk tolerance.

Through informed decision-making and strategic planning, women can unlock the full potential of their investments, ensuring a prosperous future for themselves and future generations. Here are four essential tips women must consider while investing outlined by Swati Saxena, Founder and CEO of 4 Thoughts Finance.

Improve financial literacy: Comprehending the complexities of financial products calls for strong financial literacy to avoid pitfalls. It is vital to possess knowledge of investing measures, stock types, industrial and economic cycles, and management ethics. Proficiency with digital banking and AI-powered financial tools helps in today’s environment. The ability to obtain up-to-date market data online and understand the basics of it is essential. A proficient level of financial literacy will aid the navigation of asset classes and maximize profits in an increasingly competitive environment.

Prioritizing needs and creating a comprehensive financial plan: Investments must have a rationale. They must be linked to objectives like retirement planning, economic independence, and resolving societal inequalities like the gender wealth gap. It’s also essential to save and increase income from investment because disposable income from static sources determines wealth. A clear understanding of risk and personal risk tolerance aids confident investing. Safer options like high-interest savings accounts and riskier ones like individual stocks must be prioritized based on understanding the risk as it suits the investor. It is also essential to review and monitor investments regularly.

Strategize and diversify investments: Investing across a broad range of assets reduces risk by reducing the effect of market volatility. Include mutual funds (note that mutual funds are a basket representing assets, but are themselves not an asset class), stocks, bonds, and insurance. Consult financial professionals to make well-informed judgments and avoid hurried investments. Customization is essential, including a wide choice of inexpensive, tax-efficient investments based on one’s financial condition, risk tolerance, goals and ambitions. Gains and stability are balanced by reducing overall portfolio risk through diversification across asset classes, industries, and geographies. This approach uses market possibilities for optimum returns and resilience against economic fluctuations, even as it synchronizes investments with long-term goals.

A guide for financial well-being: Handling market fluctuations while making the best of investments takes knowledge and expertise that involves effort. An experienced financial advisor provides objective fiduciary guidance to minimize conflicts of interest. Long-term economic success is protected by their understanding of logical, research-backed methodologies and tax-efficient strategies. Advice from experts is crucial in complex circumstances or in optimizing efficiency. Costs and giving up control could be difficult for a person who likes to be in charge but having a professional can provide customized solutions and sound decision-making. Wise investment management to achieve financial objectives is eased by qualified financial experts.

The growing involvement of women in the investment environment is critical in the movement toward financial emancipation and independence. Women may successfully negotiate the difficulties of investing, secure a prosperous future for themselves, and promote greater economic inclusivity by emphasizing financial knowledge, strategic planning, diversification, and seeking mentorship.

Stalin said the clearances will be given under a single window system. The Chief Minister said the projects are proposed to be set up across the state so that there is a distributed growth…reports Asian Lite News

Several MoUs with an investment intention of Rs.664,180 crore have been inked between the Tamil Nadu Government and various industrial groups, said Tamil Nadu Chief Minister MK Stalin.

Speaking at the valedictory function of the Tamil Nadu Global Investors Meet, Stalin said the state has attracted investment proposals from varied sectors like automobiles, Electric Vehicle (EV), aerospace, Defence, footwear and others.

Stalin said the investment proposals can generate about 26.90 lakh direct and indirect employment opportunities.

He also said the government will take special effort to convert the MoUs into actual projects and a special group headed by Industries Minister TRB Rajaa and senior officials will look into it.

Stalin said the clearances will be given under a single window system. The Chief Minister said the projects are proposed to be set up across the state so that there is a distributed growth.

#TNGIM2024-ஐ இந்தியாவே வியக்க வெற்றிகரமாக நடத்திக்காட்டிய மாண்புமிகு தொழில்துறை அமைச்சர் முனைவர் @TRBRajaa, அரசு உயர் அலுவலர்கள் உள்ளிட்ட அனைவருக்கும் நன்றி!

இருநாள் மாநாடு – 20 ஆயிரம் தொழில்துறைப் பிரதிநிதிகள் பங்கேற்புடனும், 39 லட்சம் மாணவர்கள் பார்வையிடவும் பல புதுமைகளோடு… pic.twitter.com/AmrWizWiD2

Giving an overall sector-wise break-up of the MoU’s, Stalin said the investment from the manufacturing sector was about Rs.3.79 lakh crore; energy Rs.1.35 lakh crore; Information Technology and Digital Services Rs.22,130 crore; MSMEs Rs.63,573 crore and others.

Some of the mega investment proposals are from the Adani Group Rs.42,768 crore (Adani Green Rs.24,500 crore, Ambuja Cements Rs.3,500 crore, Adani Connex Rs.13,200 crore and Adani Total Gas & CNG Rs.1,568 crore); Tata Power Renewable Energy about Rs.71,000 crore; Chennai Petroleum Corporation Rs.17,000 crore; Leap Green Energy Rs.22,842 crore; SembCorp Rs.36,238 crore; Salcomp Manufacturing India Rs.2,271 crore; Boeing (to set up global capability centre) Rs.309 crore; Ashok Leyland Rs.1,200 crore; Stellantis EV Rs.2,000 crore; Eicher Motors Rs.3,000 crore; Sify Technologies Rs.2,500 crore; JAM Infra (Jindal Defence) Rs.1,000 crore; Saint Gobain Rs.3,400 crore and several others.

Adani’s Mega Investment plans in Tamil Nadu

The multi-business Adani Group has decided to invest a whopping Rs 42,768 crore in Tamil Nadu in renewable energy, cement manufacturing, data centre, city gas distribution and generate 10,300 employment opportunities.

The Group announced this decision during the Tamil Nadu Global Investors Meet 2024 held on Monday.

A Memorandum of Understanding (MoU) was also exchanged at the investors’ meeting by Karan Adani, Chief Executive Officer of Adani Ports and SEZ Limited (APSEZ) and the Tamil Nadu government.

The break-up of the investments by different Adani group companies are as follows: Adani Green Rs 24,500 crore (employment 4,000), Ambuja Cements Rs 3,500 crore (5,000), Adani Connex Rs 13,200 crore (1,000) and Adani Total Gas & CNG Rs 1,568 crore (300).

German Chancellor Olaf Scholz attends a press conference with visiting French President Emmanuel Macron at the German Chancellery in Berlin, capital of Germany, May 9, 2022. (Xinhua/Ren Pengfei/IANS)

The compact with Africa is based on the initiative launched by the German government whilst chairing the G20 group of leading sovereign nations…reports Asian Lite News

The German government pledged to invest four billion euros into green energy projects in Africa until 2023, with German Chancellor Olaf Scholz saying that African countries should reap greater reward from their raw materials.

The pledge was announced at a news conference at the G20 Compact with Africa summit in Berlin. Scholz did not mention any specific projects but said the materials used in green energy should be processed in the African nations they come from, Euronews reported.

“This creates jobs and prosperity in these countries,” Scholz was cited as saying. “And the German industry gets reliable suppliers.”

The compact with Africa is based on the initiative launched by the German government whilst chairing the G20 group of leading sovereign nations.

The Compact with Africa includes Egypt, Ethiopia, Benin, Burkina Faso, Ivory Coast, Ghana, Guinea, the Democratic Republic of Congo, Morocco, Rwanda, Senegal, Togo and Tunisia.

It aims to improve the economic conditions of developing countries and to make them more attractive to foreign private investment.

“Africa is our partner of choice when it comes to intensifying our economic relations and moving toward a climate-neutral future together,” Scholz said.

When asked about China’s influence in the African continent, several African leaders said it was open to other partnerships.

“Perhaps China was more audacious, perhaps they have more vision and perhaps they trusted the potential in Africa,” Moussa Faki, the chairperson of the African Union Commission, said.

“The African continent is open to different partnerships,” he added. “We wish for you to place your trust in us, to impose less conditions and create the conditions together.”

“Improving governance, that’s our responsibility, and therefore this shared vision could allow, I’m certain of it, for a large capital that could be invested in the continent,” Faki said according to a CNN report. (ANI)

The Open RAN-compliant radio market to date has been dominated by Asian vendors Samsung, NEC and Fujitsu…reports Asian Lite News

Mobile operators are likely to invest more than $30 billion in open RAN networks globally by 2030, representing a CAGR of 24 per cent for the period, according to a latest report.

Open RAN stands for open radio access network. An open RAN is made possible by a set of industry-wide standards that telecom suppliers can follow when producing related equipment.

Open RAN network investments have increased steadily in recent years, driven primarily by greenfield network operators in the Asia-Pacific and North American regions, according to Counterpoint Research.

However, following this period of rapid network build-outs, greenfield operators are looking to lower capex in 2023 and 2024 and focus on network monetization.

Some Tier-1 operators, notably Vodafone, have announced major plans recently to deploy open RAN, but most brownfield network operators remain very cautious about additional investments in 5G infrastructure, particularly Open RAN, due to the uncertain macroeconomic climate.

As a result, the Open RAN market will stagnate during this and the next year.

“Investments will start to increase YoY after 2025 with network operators investing a cumulative total of more than $30 billion between 2022 and 2030,” the report noted.

Although the Asia-Pacific and North American regions will remain the largest Open RAN markets for most of the forecast period, Europe is expected to record the fastest growth with a CAGR of 108 per cent between 2023 and 2030 as its Tier-1s finally start commercial deployments at scale, driven partly by the need to replace legacy Chinese 3G and 4G networks.

The Open RAN-compliant radio market to date has been dominated by Asian vendors Samsung, NEC and Fujitsu.

However, Counterpoint Research expects that their market share will be impacted during the forecast period as other incumbents start offering Open RAN-compliant solutions.

Mr Adesina was speaking in a video message to participants at the 5th Africa Resilience Forum, which is being held in Abidjan from 3 to 5 October…reports Asian Lite News

The President of the African Development Bank emphasized the critical importance of prioritizing peace and security in Africa within investment decisions during a forum dedicated to enhancing the resilience of the continent’s nations and populations.

“The Africa Resilience Forum is a call to action to work together and make a transition from policy dialogue to investment, and then from investment to impact,” said Dr. Akinwumi Adesina, President of the African Development Bank Group.

Mr Adesina was speaking in a video message to participants at the 5th Africa Resilience Forum, which is being held in Abidjan from 3 to 5 October. The theme of this year’s Forum is “Financing Security, Peace and Development for a Resilient Africa”.

“We need to reverse current trends and establish an alliance of partners so that we can adopt a new investment approach that favours peace,” he said. “This will truly change the development-peace-security paradigm on our continent.”

Marie-Laure Akin-Olugbade, the African Development Bank Group’s Vice President for Regional Development, Integration and Business Delivery, emphasised that “by adopting peace-based actions, we can actually eliminate violence.”

“As development actors, we must put the communities we serve at the heart of our actions,” she continued, noting that the Bank was the first development finance institution to incorporate the issues of peace and fragility into its programmes. The institution has a Strategy for Addressing Fragility and Building Resilience in Africa (https://apo-opa.info/3KNLlGe), the aim of which is to bring an end to, in particular, the “triangle of disaster” – rural poverty, youth unemployment and environmental degradation – mentioned by Dr. Adesina in his speech.

There is a need for innovative approaches to financing peace, security and development in African countries that find themselves in situations of fragility, sometimes driven by conflict. This can only be achieved through governments, the private sector, civil society and development partners cooperating closely, say the Bank’s leaders.

As part of this commitment, the African Development Bank is working with the African Union and the continent’s Regional Economic Communities to develop Security-Indexed Investment Bonds (SIIBs), which will require a minimum of US$5 billion dollars by 2030. SIIBs offer a holistic investment strategy that combines peacebuilding and development expertise to offset the fiscal implications of high security sector spending.

Noura Hamladji, Deputy Assistant Administrator of the United Nations Development Programme (UNDP) Africa Bureau, said a coordinated approach should be taken to addressing humanitarian, developmental, peace and security needs. “Development aid, aid for income-generating activities for communities affected by conflict, and the establishment of basic social infrastructure (schools, health centres, water and sanitation) are just as valid as humanitarian action,” she said during a panel discussion. “We need massive investment in countries in conflict.”

Gilles Carbonnier, Vice President of the International Committee of the Red Cross (ICRC), welcomed the burgeoning partnerships between development finance institutions and humanitarian actors, pointing to the agreement between the ICRC and the African Development Bank to strengthen the resilience of communities in the Sahel, especially in Niger, Chad and Mali. “Hope has created an environment that is conducive to peace,” he said. “In conflicts, we must protect civilians, but also infrastructure (schools, health centres, etc.) that constitutes a public asset.”

The African Development Bank signed a Peace Financing Facility with the peacebuilding organisation Interpeace at the Forum. “There are children who are born and grow up in refugee camps, where they become adults – all these people ask of us is to lead a normal life,” said Elhadj As Sy, a member of the governing board of Interpeace.

Nearly 200 people – humanitarians, development, peace and security actors from the public and private sectors, politicians, investors, academics and members of civil society – are attending the Africa Resilience Forum in person, which can also be followed by videoconference.

Defence Minister of Vietnam, General Phan Van Giang called on President Droupadi Murmu at Rashtrapati Bhavan, according to a press release by the President’s Secretariat on Monday…reports Asian Lite News

India’s Consul General in Ho Chi Minh City, Vietnam, Madan Mohan Sethi highlighted the cordial and friendly relationship between India and Vietnam, emphasizing their historical ties through civilization that spans over 2,000 years.

“More than 400 Indian companies, small and big have invested in Vietnam for a cumulative value of more than USD 1 billion,” he said.

He mentioned that both countries have collaborated in various areas, including trade, defense, and strategic cooperation.

He noted the increasing number of Indian tourists visiting Vietnam, with over 400,000 Indian tourists estimated to have visited the country in recent times.

“As far as the relationship between India and Vietnam is concerned, both countries enjoy a very cordial and friendly relationship,” Sethi said.

He said the two countries have a “historical connection through culture and civilizational roots going back to more than 2000 years. In recent times, we have cooperated with Vietnam in multiple areas including trade and commerce, defence and strategic areas.

He also mentioned a growing interest among Vietnamese travelers to explore India.

“But from last year June onwards, with more connection between cities like Ho Chi Minh City and Hanoi, with our cities of India like Kolkata, Delhi, Mumbai, Ahmadabad and very recently Kochi, what we are witnessing that hundreds of Indian tourists are visiting Vietnam,” the Consul General said.

“So by one estimate, I think more than 400,000 Indian tourists have already visited Vietnam and we are also seeing a surge in the number of Vietnamese travelling to India,” he added.

As per Sethi, Vietnam has a relationship with India through yoga and Buddhism. “Nowadays we are promoting the Vietnamese provinces to visit Indian states to develop partnership and cooperation in multiple areas including higher education, IT, healthcare and tourism.”

He said: “India’s image has changed a lot in recent times due to the steps by the government of India under PM Modi. And perhaps more engagements have been made with a large number of countries in the last nine years. …But definitely there is more intense engagement with the countries, with our friendly countries and again countries of the south actually.”

Recently, the Defence Minister of Vietnam, General Phan Van Giang called on President Droupadi Murmu at Rashtrapati Bhavan, according to a press release by the President’s Secretariat on Monday.

Welcoming General Giang and his delegation to India, the President said that India and Vietnam share a rich history of civilizational and cultural linkages spanning over 2000 years.

She added that Vietnam is an important pillar of India’s Act East Policy and a key partner of our Indo-Pacific Vision.

President Murmu noted that the India-Vietnam ‘Comprehensive Strategic Partnership’ has widened the range of bilateral collaboration including in defence and security cooperation, trade and investment relations, energy security, development cooperation, cultural and people-to-people relations. (ANI)